Long COVID is a range of prolonged symptoms after a COVID infection. It can include brain fog, fatigue, gastrointestinal issues—not to mention anxiety and depression. But there can also be some financial side effects: high out-of-pocket costs and medical debt.

Fifteen months after getting COVID, Becca Meyer from Kalamazoo is still dealing with some serious side effects. She’s also trying to manage the financial burden of Long COVID.

She has four kids and she can’t work because she’s sick. Her partner was laid off, too.

“Any extra money we've had like [our] tax return or stimulus check has all gone to medical debt,” Meyer said. “We don’t purchase anything fun, we purchase medications.”

Meyer doesn’t actually know how much medical debt she has, but the last time she checked she thinks it was $10,000. She stopped opening some of her bills.

“It's not the smartest choice, but I can't pay them with fake money, so why open it?”

There are a few reasons why Meyer has such huge costs. The first being she needs a lot of care. She was recently diagnosed with post-COVID generalized GI dysmotility, which is why she needs a feeding tube. Meyer also needs anti-nausea medicines because she’s throwing up all of the time.

On a regular basis she sees a chiropractor, a therapist, and her primary care doctor. And then there’s her teeth.

“I have a huge dental bill,” Meyer said. “I have to pay $6,200 to get my teeth fixed because throwing up every day for 15 months is really not good for your teeth.”

Now here’s the real root of her costs: her insurance doesn’t cover all of it. She has a cap on certain doctor visits that are covered and some of her doctors are out of network. She says some medicines aren’t covered either.

You may be thinking, why doesn’t she just change her insurance? She’s tried, but bureaucracy is slow. So she’s just waiting until she has the green light to switch her plan. Until then, it’s piling unopened bills, asking for community support, and charging credit cards.

Heather-Elizabeth Brown is another Long COVID patient. She lives in Detroit and got COVID back in April 2020.

Brown is dealing with health issues, like COVID induced diabetes, pulmonary problems, and lymphedema. She’s had to exercise a lot of self advocacy over the past 14 months to get the care she needs.

“Even when I see higher price tags on things, I make the decision to go ahead and get the treatment or see this doctor or get this supplement or go to this therapy session and then look at my finances and try to find a way to make it work,” Brown said.

Back in June 2020, Brown had to go to the hospital for an in-patient physical therapy stay. She had blood clots after COVID and couldn’t walk. She’s now facing a $55,000 medical bill that her insurance won’t cover.

“As far as my plan for paying off the debt, my plan is to get my insurance to cover that $55,000 plus—to just continually go back and not accept ‘no’ as an answer.”

Five things you can do to mitigate your medical bills

Maybe you’re in a similar position as Meyer and Brown. Whether you’re struggling with medical expenses from COVID or from any other healthcare need, there are some steps you can take in approaching these bills.

Meredith Buhalis at the Washtenaw Health Plan works with people navigating the healthcare system. She has five suggestions she makes to her clients facing large medical bills.

-

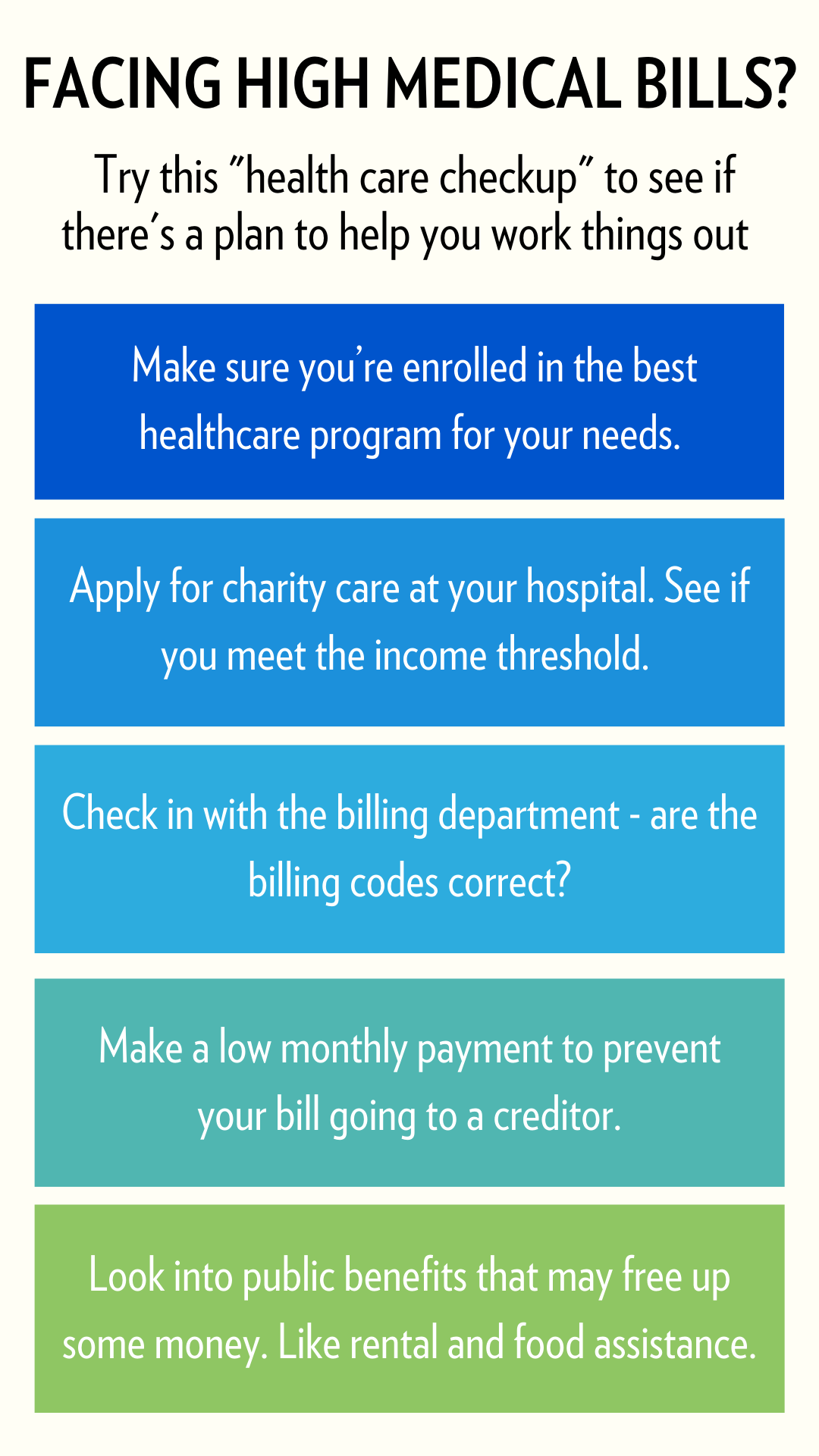

Find the best coverage

“The first thing we usually do is make sure that they have the best coverage for whatever is going on with them or the best or they are enrolled in the correct program,” Buhalis said.

Do you need to switch insurance plans to cover your doctors? Do you qualify for Medicaid? Can you make Medicaid a secondary insurance to cover some costs?

- Check in with the billing department

Did you send the bill to the right place? Was there a mistake with a billing code? Checking in with the billing department can sort out any administrative errors.

- Apply for charity care at your hospital

If you meet a certain income threshold, charity care can help.

“Charity care can cover sometimes prescriptions, co-pays, deductibles, out-of-pocket costs that are not covered by your insurance,” Buhalis said.

- Make a low monthly payment

A lot of people in medical debt fear that their bill will go to a creditor. “You can always offer to pay as low as five dollars a month,” Buhalis said. This can often stop the creditor process.

- Apply for public benefits

Look into public benefits, like rental and food assistance. If you’re cutting costs in other areas of your life, you can free up some money for medical needs.

Buhalis says she’d be happy if her job didn’t exist. Not because she doesn’t like her job, but because it would mean real change.

“It's 2021. Let's all join the rest of the world with socialized medicine and treat this as what it is: a human right.”

Out-of-Pocket Costs for COVID are common

Dr. Kao-Ping Chua is a general pediatrician and health services researcher in the Department of Pediatrics and the Susan B. Meister Child Health Evaluation and Research Center at the University of Michigan. He’s been studying the out-of-pocket costs of COVID.

Chua’s study found that a lot of people hospitalized with COVID were on the hook for some of those expenses. According to his study, 71.2% of privately insured and 49.1% of Medicare Advantage patients had out-of-pocket costs. That’s in spite of claims from many insurance companies that they would waive the costs of initial COVID hospitalizations.

So what ended up happening is that some people were already in medical debt before they developed long COVID. When these symptoms did start, the medical bills just kept piling up.

Chua found that about one in 10 patients who have Medicare Advantage insurance and about one in 14 privately insured patients had to pay over $2,000 within 90 days of discharge from a COVID hospitalization.

Now, in 2021, insurance companies are abandoning those hospitalization waivers. Chua thinks the federal government should mandate full coverage for COVID hospitalizations. At least while the U.S. is still in a public health emergency. But as for covering long term COVID care, the kind of care Long Haulers need, Chua doesn’t see that happening

“If you do that for COVID patients, then patients with other chronic diseases who also have to spend a lot, then they'll start saying, well, why not me?” Chua said.

COVID has exposed so many of the contradictions within our healthcare system. Being sick is expensive. It’s not a new reality—but the sheer number of people who have been hospitalized because of COVID, the sheer number of people who need post-COVID care—that is new. That’s our new reality.

Want to support reporting like this? Consider making a gift to Michigan Radio today.